- GCash IPO: Why Your Mobile Wallet Is About to Become a Stock Market Heavyweight

- The Numbers: A Mega-IPO In Pesos

- The Share Breakdown (For Those Who Care About Details)

- When Is The IPO Happening?

- Retail vs Institutional: Here’s Where Your Allocation Comes From

- Why GCash, And Why Now?

- The Financial Reality Check

- Where The Money Actually Comes From

- Why Now? Because Globe Can’t Hide The Value Anymore

- The PSEi Wild Card: Will GCash Reshape Index Rules?

- Why This Actually Matters For The Whole Market

- Tech Patrol Insight: Why This Matters For Filipinos

- Where To Buy GCash Stocks (When It Lists)

- With Affiliate Links

- Major Brokers (No Affiliate)

- What Happens If You Want To Invest

- Step-By-Step Tutorial: How To Buy GCash Shares

- Here’s The Full Timeline You’ll Experience:

- The Allocation Reality

- What To Expect After You Buy GCash Shares

- The Bigger Picture: What This Means For The Fintech Industry

- The Risks Nobody’s Talking About (But The Prospectus Is)

- Regulatory Risk: The Gambling Link Removal

- CreditTech Growth Dependence

- Competition Is Getting Serious

- The Merchant Ecosystem Risk

- Final Thoughts: History In Motion

- SOURCES

- FTC Affiliate Disclosure

GCash IPO: Why Your Mobile Wallet Is About to Become a Stock Market Heavyweight

You’re scrolling through your GCash app at 2 AM, checking if your offshore freelance payment came through. It did. You smile. For millions of Filipinos, GCash isn’t just an app—it’s freedom from bank queues, OFW survival kit, and the entire cashless future wrapped in a smartphone.

Now, here’s what’s happening: GCash is going public, and it’s about to rewrite Philippine stock market history.

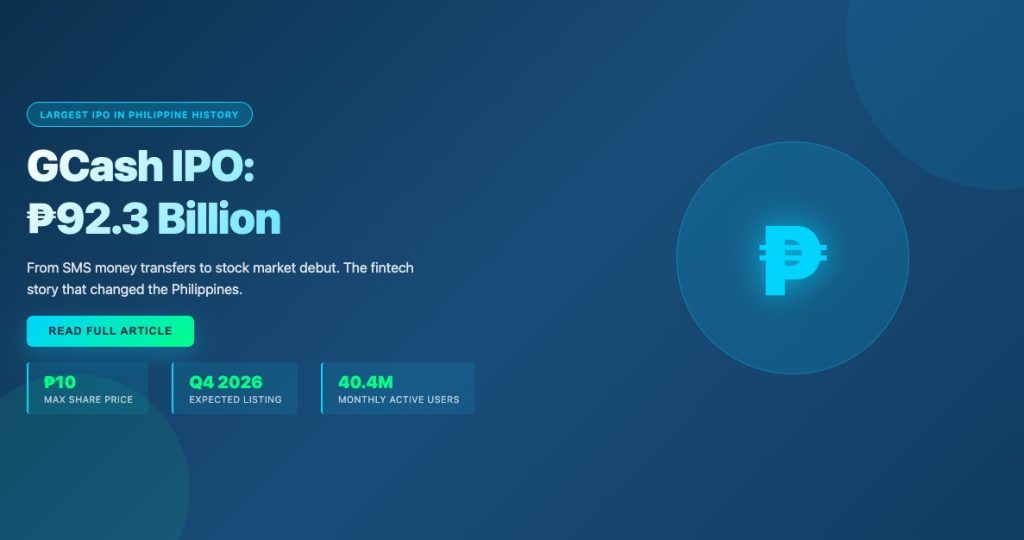

On June 27, 2026, Mynt Inc.—the company that owns GCash—officially filed its IPO registration with the Philippine Securities and Exchange Commission. What you’re looking at is not just another fintech listing. This is the largest initial public offering in Philippine history, with plans to raise as much as ₱92.3 billion ($1.5 billion), surpassing Monde Nissin Corp.’s 2021 record of ₱48.6 billion.

Let’s break down what this IPO actually means for you, your money, and the future of digital finance in the Philippines.

The Numbers: A Mega-IPO In Pesos

Here’s where it gets interesting—and slightly mind-bending.

Mynt plans to offer up to 9.23 billion shares at a maximum price of ₱10 per share, representing a 13.8 percent stake in the company. If you’re trying to do the math in your head: yes, that’s ₱92.3 billion in potential proceeds. In US dollars, that’s roughly $1.5 billion—a figure so massive it makes you wonder how the Philippine Stock Exchange (PSE) is going to handle the liquidity shock.

But here’s the real kicker: Based on the prospectus filing, Mynt’s implied valuation at the maximum share price of ₱10 sits around ₱669 billion, which translates to approximately $11.4 billion USD at current exchange rates.

To put that in perspective, Mynt is already being valued higher than most Philippine conglomerates that have been listed for decades. Your Viber group chat might break when this IPO news drops—and that’s not an exaggeration.

The Share Breakdown (For Those Who Care About Details)

The IPO isn’t just one simple offering. The prospectus reveals a critical detail that changes how you should think about this deal.

Base offer: Up to 8.03 billion shares

- 1.61 billion = primary shares (newly issued—fresh money to Mynt)

- 6.42 billion = secondary shares (existing shares from current shareholders)

- Overallotment option: 1.2 billion additional shares (all secondary)

Here’s the brutal truth: roughly 80 percent of the IPO consists of secondary shares, meaning most of the ₱92.3 billion in gross proceeds will go to Globe Telecom, Ant Group, Ayala Corporation, and other existing shareholders—not to Mynt itself.

Of the ₱80.3 billion base offering, only about ₱14.9 billion in net proceeds will actually flow to Mynt from newly issued primary shares. The remaining ₱74.3 billion (assuming full overallotment) goes to shareholders taking money off the table.

The primary shares Mynt retains will fund three areas: expansion of its CreditTech business (its fastest-growing division), product development, strategic cash reserves, and general corporate purposes. Translation: GCash’s lending arm is about to get a major capital injection.

What does that mean in real-people terms? When you see Globe Telecom and Ant Group making billions from this IPO, that’s them partially cashing out their GCash stakes. It’s not necessarily a bad thing—it’s just important to know that you’re buying a company where existing shareholders are taking profits, not a company where management is doubling down on its own conviction.

When Is The IPO Happening?

This is where patience comes in. The proposed offering is expected to happen in the fourth quarter of 2026—so sometime between October and December this year.

According to the prospectus filing, here’s the expected timeline:

- Indicative Pricing Date: Around September 28, 2026

- Expected Retail Settlement: Around October 9, 2026

- Official Listing: Sometime in Q4 2026 (post-settlement)

That timeline feels both forever away and impossibly close, depending on whether you’re holding GCash shares or just wanting to buy some. The good news: there’s still time for the SEC to review the filing, for the market to absorb the news, and for GCash users (all 94 million of you, with 40.4 million monthly actives) to slowly realize that your favorite fintech app is about to become a publicly traded company.

The bad news: if market conditions turn south—which they absolutely can—this IPO could get pushed into 2027. That’s the uncertainty baked into the announcement.

Retail vs Institutional: Here’s Where Your Allocation Comes From

The prospectus reveals a critical detail about how shares will be distributed. Of the ₱80.3 billion base offering (before overallotment):

- 70% allocated to institutional investors (pension funds, insurance companies, foreign funds)

- 30% allocated to retail and trading participants (you and regular investors)

- 20% through brokers (COL Financial, PhilStocks, etc.)

- 10% reserved for Local Small Investors (retail investors with smaller budgets)

This is important because it means retail demand will be competed for. If institutional appetite is sky-high, your allocation might get cut even if you apply.

Why GCash, And Why Now?

Here’s the story that matters. GCash didn’t start as a fintech unicorn. It grew from a text-based money transfer service launched in 2004 into the country’s largest mobile wallet, with 40.4 million monthly active users as of March 31, 2026 (and 94 million registered users across its lifetime).

Think about that trajectory: SMS-based remittances in 2004 → dominant digital payments app in 2026 → publicly traded megalith in late 2026.

The Financial Reality Check

The prospectus tells a story of explosive growth. For the full year 2025, Mynt posted ₱79.8 billion in revenue and ₱17.2 billion in net income. To put that in perspective, here’s the three-year trajectory:

| Year | Revenue | Net Income | Growth |

|---|---|---|---|

| 2023 | ₱33.6B | ₱6.38B | — |

| 2024 | ₱54.1B | ₱11.13B | +61% revenue, +74% profit |

| 2025 | ₱79.7B | ₱17.25B | +47% revenue, +55% profit |

| Q1 2026 | ₱20.74B | ₱5.6B | +23% YoY net income |

This isn’t just growth—this is the kind of trajectory that makes hedge funds lose sleep.

Where The Money Actually Comes From

Payment volume remains the company’s biggest strength: ₱17.03 trillion in payment solutions gross transaction value (GTV) in 2025, with ₱4.75 trillion GTV during the first quarter of 2026 alone, up 23.2 percent year on year.

But here’s the hidden story that the prospectus reveals: GCash is diversifying away from pure payments. The filing disclosed:

- 7.5 million active borrowers (lending division generating major revenue)

- 16.9 million savings account users (tapping into GSave and partner banks)

- 9 million investment fund users (including GStocks Ph for stock trading)

- 1.9 million users investing in Philippine stocks (making stock market access accessible)

This is the future of GCash. Payments are the hook—lending, wealth management, and insurance are where the profit margins live. Fuse Lending, the lending arm of Mynt, has disbursed loans worth PHP 362 billion (USD 6.16 billion) life-to-date, a substantial 65% increase from 2024, driven by over 10.5 million unique borrowers.

The new capital from the IPO (those ₱14.9 billion primary shares) is explicitly earmarked for CreditTech expansion. Translation: GCash’s lending division is about to get on steroids.

Why Now? Because Globe Can’t Hide The Value Anymore

GCash exists because OFWs needed a faster way to send money home. It became essential because of EDSA traffic—nobody wants to sit in bumper-to-bumper hell just to pay a bill. It thrived because Filipinos realized they could do almost everything through their phones: pay rent, send money to Cebu, buy load, invest, borrow, insure themselves, even trade stocks (via GStocks PH).

But here’s what finally pushed this IPO timeline: Globe Telecom’s earnings disclosure made it impossible to ignore.

Mynt’s attributable equity earnings to Globe reached ₱6.1 billion in 2025, up 64% year-on-year, and now accounts for 30% of Globe’s net income before tax. Translation: GCash has stopped being a side hustle for Globe and has become the profit engine.

The market finally realized what insiders have known for years: GCash is worth more than the entire Globe Telecom valuation suggests. A publicly traded GCash would force the market to reprice both companies correctly.

For Ant Group (Alipay’s parent, which has a major stake in Mynt), an IPO on the Philippine Stock Exchange is a clean exit from China’s regulatory storm. For Ayala Corp., it’s finally getting public credit for a business it’s been quietly backing for years.

The PSEi Wild Card: Will GCash Reshape Index Rules?

Here’s a question that no one’s talking about but everyone in the market should be: Will GCash even be allowed in the PSEi (Philippine Stock Exchange Index)?

The answer is surprisingly complicated, and it could force the PSE to change its rules for the first time in a generation.

Currently, to be included in the PSEi—the benchmark 30-member index that tracks the health of the Philippine stock market—companies must maintain a public float of at least 20 percent. GCash will only have a 12 percent public float post-IPO.

According to April Lee-Tan, chief equity strategist at COL Financial: “For Mynt to become part of the PSEi index, they would have to allow companies with a free float of less than 20 percent to be part of the PSEi.”

This matters because Lee-Tan points out that relaxing the threshold would not only pave the way for Mynt to enter the index but could also benefit other listed firms currently short of the minimum float requirement, such as AboitizPower, which could potentially rejoin the PSEi.

Why This Actually Matters For The Whole Market

If the PSE does lower the PSEi inclusion threshold to accommodate GCash, it could create a ripple effect across the market. Over the long term, if Mynt performs well in the stock market and becomes part of the index, the whole Philippine market could benefit from attracting more passive investors—institutional investors who would buy index funds that replicate PSEi performance.

Think about it this way: Philippine mutual funds track the PSEi. International index funds track the PSEi. If GCash isn’t in the index, those passive flows bypass the company entirely. But if GCash gets included, billions in automatic flows follow.

The bigger cultural shift: As Lee-Tan told the Inquirer, “For the longest time, one of the issues that investors have in the Philippines is that we are all traditional companies. We’re not part of the other markets that have tech stocks, but with the listing of GCash, it changes that.”

The PSE has been dominated by banks, property developers, telcos, and conglomerates for 30 years. GCash would be the first genuinely tech-first company at that scale. That’s not just good for GCash investors—it’s good for the entire market’s narrative.

Now here’s where the skeptics get nervous. The PSE remains one of Asia’s most illiquid markets, with daily trading activity concentrated in a limited number of blue-chip stocks, and foreign investors being one of the most significant net sellers in recent years.

What does that mean? It means the Philippine Stock Exchange has never had to absorb an IPO this massive. Imagine dumping ₱92.3 billion of GCash shares into a market that typically moves ₱6 billion a day in total trading volume. That’s roughly 15 days of normal market activity in a single transaction.

The real question haunting analysts: Will the market absorb it, or will it just rotate money from one blue-chip stock to another?

Tech Patrol Insight: Why This Matters For Filipinos

Here’s what nobody’s talking about loud enough: this IPO is a referendum on whether the Philippine capital market has grown up.

For decades, the PSE has been dominated by banks, real estate, and conglomerates—old money, old infrastructure, old stories. A successful GCash IPO wouldn’t just be about fintech. It would prove that Filipino investors are willing to bet on a company built entirely on digital services and mobile-first thinking.

It would also unlock something profound: a direct way for ordinary Filipinos to own a piece of the digital economy they’ve already been using for two decades.

GCash users are mostly unbanked or underbanked Filipinos. They use GCash because the nearest physical bank branch is in the next town over. They use it because their salaries get deposited there. They use it because their tita sends remittances through it every month. If this IPO happens, those same Filipinos could theoretically use their GCash balance to open a brokerage account and buy GCash stock. It’s beautifully recursive.

The language of finance—valuations, public floats, underwriters—feels foreign to most Filipinos. But GCash is the opposite. It’s the most Filipino fintech story there is. It’s ours.

Where To Buy GCash Stocks (When It Lists)

Once the IPO launches in Q4 2026, you’ll need a brokerage account to participate. Here are the major platforms accepting IPO applications:

With Affiliate Links

DragonFi (recommended for easy onboarding)

- Link: dragonfi.com (use code C195A for affiliate benefits)

- Known for: User-friendly app, low fees, fast account setup

- IPO allocation: Full retail access (20% broker allocation)

- How it works: Download app → KYC → Fund account → Submit IPO application

Major Brokers (No Affiliate)

COL Financial

- Known for: Extensive research tools, institutional-grade platform

- IPO allocation: Full retail access

- Good for: Experienced investors who want detailed market data

First Metro Securities

- User-friendly platform with good customer service

- IPO allocation: Full retail access

EastWest Bank Securities

- Bank-integrated (good if you have EastWest account)

- Streamlined funding process

Security Bank Online Investing

- Simple interface, integrated with Security Bank

- Good for first-time IPO participants

Maybank Securities PH

- International broker with Philippines presence

- Competitive pricing

What Happens If You Want To Invest

Let’s be practical. When—and if—this IPO prices, you won’t be able to buy GCash shares at your local SM Mall of Asia counter. You’ll need:

- A PSE-authorized brokerage account (your usual suspects: COL Financial, PhilStocks, COL, First Metro, EastWest, Security Bank, Maybank, etc.)

- Money in that account when the offering happens (application period is expected around late September 2026)

- Access to the IPO allocation during the public offering period

Step-By-Step Tutorial: How To Buy GCash Shares

Step 1: Open a Brokerage Account (If You Don’t Have One)

- Visit DragonFi.com (use code C195A for affiliate benefits) or COL Financial, First Metro, etc.

- Complete KYC (Know Your Customer): Upload ID, proof of address, selfie

- Takes 1-3 business days typically

- Pro tip: Do this NOW, not in September. Don’t wait until IPO day—servers crash.

Or, click the link below:

DragonFiStep 2: Fund Your Brokerage Account

- Transfer pesos from your bank to your broker account

- Minimum varies by broker (typically ₱5,000-₱25,000 for retail IPO participation)

- Make sure funds are cleared BEFORE the application period opens

- Best method: InstaPay or Direct Debit for instant transfers

Step 3: Watch for IPO Announcement (Late September 2026)

- Around September 28, SEC announces final pricing (expected: ₱10/share)

- Your broker opens IPO application window (usually 2-3 trading days)

- You’ll see “IPO Application” or “Public Offering” tab in the app/website

Step 4: Submit Your IPO Application

- Log into your broker account

- Navigate to IPO section

- Enter number of shares you want (multiples of 100 typically)

- Example: Want ₱50,000 worth? → 5,000 shares at ₱10 = ₱50,000

- IMPORTANT: Submit EARLY. Brokers have server limits on IPO day—don’t submit at 4:59 PM.

Step 5: Wait for Allocation (October 1-9, 2026)

- Institutional investors get allocated first

- Then retail allocations are processed pro-rata

- Broker notifies you via app/SMS/email: full allocation, partial, or zero

- Expected retail settlement: October 9, 2026

Step 6: Shares Hit Your Account

- Shares appear in your portfolio

- You can HOLD for long-term or SELL once trading begins

- First trading day typically 1-3 days after settlement

Here’s The Full Timeline You’ll Experience:

Around September 28, 2026: Indicative pricing announcement (the market finds out the actual share price)

Late September 2026: IPO application period opens (you submit your buy orders)

Around October 9, 2026: Expected retail settlement (shares credited to your account)

October-December 2026: Official listing and first trading day (you can buy/sell freely)

The Allocation Reality

The prospectus allocates 30% of shares to retail and trading participants. Of that 30%:

- 20% goes through brokers (standard retail)

- 10% is reserved for Local Small Investors (which means reduced minimum investments for ordinary Filipinos)

Here’s the catch: Even within the retail pool, IPOs are allocated on a pro-rata basis if oversubscribed. This means if 10 million Filipinos apply for shares and demand is 5x supply, you get 20% of what you requested.

This is called the “allocation lottery,” and it’s equally fair and frustrating. The good news: GCash is so dominant that unless the market completely tanks, this IPO should be oversubscribed (more demand than supply). The bad news: that means your allocation might get cut to 10% of what you requested.

Pro tip: Open your brokerage account NOW (if you haven’t already). IPO applications are first-come, first-served on the brokerage side, and technical glitches are common on application day. Don’t wait until September 27 to set up your account.

What To Expect After You Buy GCash Shares

If You Get Allocated (You’re Now a Shareholder):

- You own a piece of Mynt Inc.

- You can vote in shareholder meetings

- You’re entitled to dividends (if the company declares them)

- You can sell anytime once trading opens

- Your shares are held safely in your broker’s custodian account

Post-IPO Trading Reality:

- First 5-10 trading days = HIGH volatility (wild price swings)

- Day traders often flip shares for quick profit (risky—many lose)

- Long-term investors typically hold 3-5 years for real gains

- Don’t panic sell if price drops in first week (IPO volatility is normal)

Watch These Metrics Quarterly (After IPO):

- Net Income: Should stay profitable and growing

- Monthly Active Users: Should grow or hold steady (40.4M+ is healthy)

- GTV (Gross Transaction Value): Monthly trends matter—growth signals health

- Lending Portfolio: Watch for rising defaults (bad sign)

- Regulatory news: Any BSP announcements can move the stock

- Earnings per share (EPS): This determines if stock price is reasonable

Ask Yourself Before Buying:

- Can I afford to lose this money? (Stocks can go down)

- Am I buying for long-term wealth (5+ years) or quick flip?

- Do I understand GCash’s business model? (If not, research more)

- What price would make me sell? (Set your exit plan beforehand)

The Bigger Picture: What This Means For The Fintech Industry

If Mynt’s IPO succeeds—and succeeds well—you’ll see a cascade of imitators. Filipino startups will point to GCash and say, “If they can go public at a ₱464 billion valuation, why can’t we?”

That’s a good thing. It means capital will start flowing into technology and fintech. It means the PSE will finally have a tech story to tell. It means a generation of Filipino engineers and product managers will have a path to wealth that doesn’t require moving to Silicon Valley.

But there’s a flip side. If this IPO merely rotates domestic funds among existing listed companies rather than attracting fresh foreign capital, the success will be more symbolic than transformative. A true market victory would mean new money flowing into the Philippines, not just existing pesos moving between stock accounts.

Related story: GCash valuation soars to 5B USD

The Risks Nobody’s Talking About (But The Prospectus Is)

Here’s where the article gets uncomfortable, because every IPO prospectus is required to list all the ways the company could fail. The GCash prospectus is no exception, and it reveals some real vulnerabilities that investors should know about.

Regulatory Risk: The Gambling Link Removal

The prospectus specifically references the Bangko Sentral ng Pilipinas (BSP) directive requiring removal of gambling links from payment apps in 2025. This is a real example of how regulatory actions can affect revenue streams. GCash has dependencies on gaming and entertainment platforms for a portion of its transaction volume. If future regulations tighten, that revenue could evaporate overnight.

Translation: Regulators can change the rules of the game at any time, and GCash’s business model depends partly on regulatory tolerance.

CreditTech Growth Dependence

The prospectus highlighted that a significant portion of future growth is expected to come from CreditTech (its lending division). This is critical because lending is more profitable than payments, but it also carries higher default risks. Loan quality will be an important metric to watch post-IPO.

If Fuse Lending (GCash’s lending arm) suddenly faces a wave of defaults—say, because of an economic recession or inflation crisis—earnings could collapse faster than a jeepney on EDSA during rush hour.

Competition Is Getting Serious

The prospectus acknowledges risks from digital banks, e-wallets, and other fintech platforms. GCash is dominant today, but maintaining leadership against competitors like:

- Maya (formerly PayMaya)

- Emerging digital banks (BPI Digital, BDO Digital)

- International fintech platforms entering the Philippine market

…remains a key challenge.

The prospectus also noted that if GCash gets disrupted by new technology or consumer preferences shift (maybe Gen Z prefers something built on blockchain, who knows?), the company could lose market share faster than expected.

The Merchant Ecosystem Risk

GCash’s strength is its 2.1 million QR merchants and 1.3 million cash-in/cash-out locations. But these relationships are not exclusive. A merchant can accept Maya, GCASH, and PayMaya simultaneously. If those merchants suddenly decide GCash is less valuable to their business, they can deprioritize the service overnight.

Final Thoughts: History In Motion

In a few months, you might walk into a BDO branch and see a GCash billboard advertising IPO applications. You’ll see TikTok creators explaining what public float means. You’ll hear titos and titas arguing about whether GCash is overvalued at ₱669 billion (spoiler: some will say yes, some will buy anyway).

Here’s the honest take: You’re not buying a pure growth story. You’re buying a company with 40.4 million monthly active users, ₱79.8 billion in annual revenue, and ₱17.2 billion in net income. Those are the numbers of a mature, profitable business—not a startup. The growth is still impressive (47% revenue growth in 2025), but this isn’t a moonshot bet anymore.

The real miracle isn’t the ₱92.3 billion IPO size. It’s that a service born from the very Filipino problem of “how do I send money home without going to a bank” has become a company worth ₱669 billion.

But here’s one more thing to remember: Roughly 80% of the IPO proceeds go to existing shareholders cashing out. That’s not necessarily bad—it’s just important context. Globe Telecom, Ant Group, and Ayala are taking profits here. They still believe in GCash (they’re keeping 88% of their stakes), but they’re also saying “we’ve had enough exposure, let’s diversify.”

The target listing window is the fourth quarter of 2026, which gives Mynt several months to finish registration work and test institutional appetite. Between now and then, the headlines will build. The speculation will grow. And millions of GCash users will realize that the app they’ve been using to pay their electric bill is about to become the biggest stock market debut in the country’s history.

That’s not just a stock market story. That’s the Philippines’ digital future finally getting priced by the market.

The PSE better be ready—and it better adjust its rules to accommodate the company that’s actually reshaping Philippine finance.

UPDATE FOR INVESTORS: The SEC filing was officially submitted on June 27, 2026. This is not speculation anymore. This is happening.

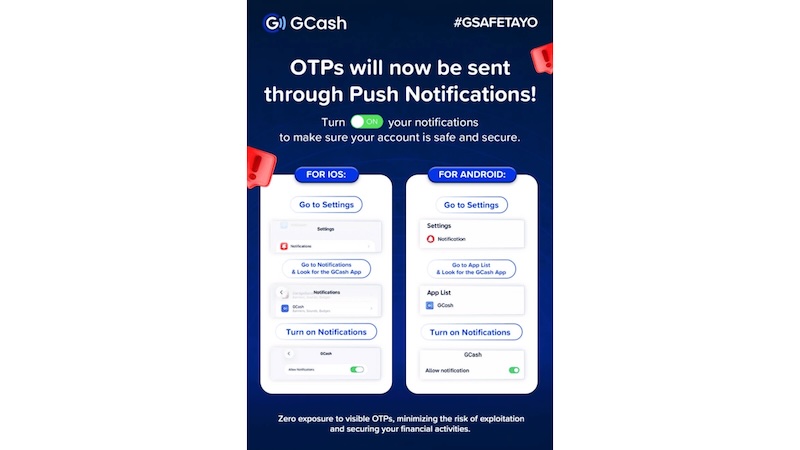

Related: GCash In-App OTP Rollout 2026: Push Notifications Replace SMS for Better Security

SOURCES

- Manila Bulletin – “GCash parent Mynt plans ₱10-a-share mega IPO”

https://mb.com.ph/2026/06/26/gcash-parent-mynt-plans-10-a-share-mega-ipo

- Insider PH – “GCash parent Mynt advances PSE IPO with SEC registration filing” (includes prospectus data)

https://insiderph.com/gcash-parent-mynt-advances-pse-ipo-with-sec-registration-filing

- Business Inquirer – “GCash IPO seen reshaping PSEi rules”

https://business.inquirer.net/597244/gcash-ipo-seen-reshaping-psei-rules

FTC Affiliate Disclosure

This article contains affiliate links. Tech Patrol may earn a commission if you open a brokerage account through the DragonFi affiliate link (code: C195A) or other broker links mentioned. This does not affect the price you pay—it’s how we support independent tech journalism in the Philippines. We only recommend brokers we believe are legitimate and user-friendly. All opinions about GCash and the IPO are our own, based on publicly available prospectus data and market analysis.