Introduction

PERA vs Pag-IBIG MP2 turns into an actual argument the moment thirteenth month pay lands in your account.

Group chat explodes. Kuya sends a screenshot. Tita sends a Facebook post with three exclamation points. Everyone suddenly has an opinion, and none of them agree.

Two programs. One bonus. Zero clarity.

Both promise growth. Both carry a government seal. Both get thrown around like they’re the same thing, the way “Xerox” gets used for every photocopier. They are not the same thing.

Pick wrong, and your money sits locked up for years, moving slower than an EDSA jeepney at rush hour. Pick right, and that bonus goes to work instead of just disappearing into GCash like everything else does.

This guide breaks PERA vs Pag-IBIG MP2 down in plain terms. No jargon. No sales pitch. Just the numbers, the rules, and which one fits your actual situation.

The Problem

Here’s what usually happens.

Someone hears MP2 paid 7.12% last year. Someone else hears PERA hands out a 5% tax credit. Numbers get compared like a title fight. Bigger number wins, right?

Wrong. Retirement planning is not a slugfest, no matter how much your group chat wants it to be one.

But here’s the real issue: these two accounts don’t work the same way at all. One is a fixed five-year savings program. The other is a full investment account with actual market risk attached.

Mix up the two, and the mistakes get expensive. Lock ₱200,000 into a five-year MP2 term, then need it back for an emergency in year three, and you’re forfeiting half your dividends. Dump your entire bonus into PERA equities expecting MP2-style stability, then panic when the market has a rough quarter.

Neither mistake is fun. Both are avoidable, once you understand what each account is built to do.

Solution

Here’s where it gets interesting. These two programs were never built to compete. They solve two different problems.

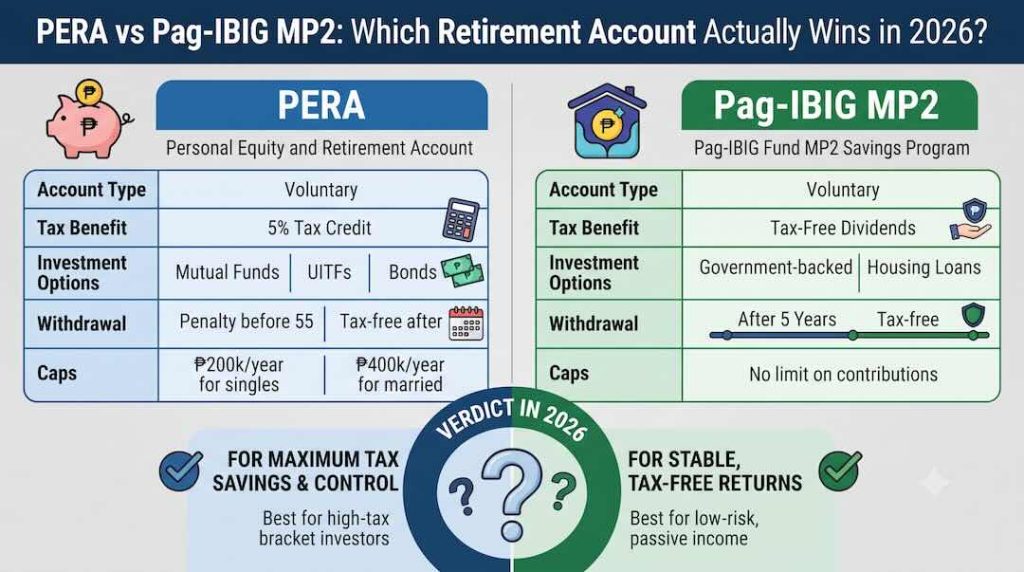

What Pag-IBIG MP2 Actually Is

Modified Pag-IBIG 2, or MP2, is a savings program. Not an investment account. A savings program with better-than-average dividends.

Any active Pag-IBIG member can open one. That’s most working Filipinos already, since Pag-IBIG membership usually comes bundled with employment.

Contribute at least ₱500. Less than your monthly Netflix-Spotify-Disney combo, and unlike that combo, this one pays you back.

Choose a fixed five-year term. Pick compounded growth or annual payout. Then wait.

Pag-IBIG declares a dividend rate every year, based on actual fund performance. For 2025, that rate hit 7.12%, up from 7.10% in 2024. The highest dividend declaration in the fund’s 45-year history.

Dividends are also tax-free. A 2025 Department of Finance clarification confirmed it directly: savings in SSS, GSIS, and Pag-IBIG, MP2 included, stay untaxed.

One catch worth remembering. That 7.12% isn’t a locked-in promise. Pag-IBIG only knows the real number after the year closes, since it’s not in the business of psychic predictions. Next year’s rate could climb higher. It could also drop. It moves with performance, not with guarantees.

What PERA Actually Is

PERA stands for Personal Equity and Retirement Account, established under Republic Act No. 9505. Built specifically for retirement, not general savings.

This is where the real difference shows up. With PERA, you choose the underlying investment yourself. Government bonds. PSE-listed stocks. REITs. UITFs. Conservative or aggressive, entirely your call.

Every contribution earns a 5% tax credit, applied directly against your income tax due. Local contributors can put in up to ₱200,000 a year for up to ₱10,000 back. OFWs get double the room: ₱400,000 in contributions, ₱20,000 in tax credits.

Growth inside PERA is tax-free too. Dividends, interest, capital gains, none of it gets taxed while it stays in the account.

The catch is patience, and a lot of it, more patience than waiting for a jeepney to fill up during a sudden downpour. You need to hit 55 years old, with at least five years of contributions, before you can withdraw tax-free. Pull the money out early, and you generally forfeit the tax credit and pay back what the BIR waived.

Related: PERA Philippines: The Retirement Account That Pays You Back Starting Today

Side by Side

| Pag-IBIG MP2 | PERA | |

|---|---|---|

| What it is | Government dividend savings program | Investment account, you pick the funds |

| Minimum contribution | ₱500 per remittance | No fixed minimum |

| Maximum contribution | No cap (lump sums over ₱500,000 need a Manager’s Check) | ₱200,000/year (local), ₱400,000/year (OFW) |

| Government incentive | Tax-free dividends, no upfront credit | 5% tax credit on contributions, upfront |

| 2025 return | 7.12% declared dividend rate | Depends entirely on chosen fund |

| Risk level | Low, government-backed, declared rate | Varies, from conservative bonds to aggressive equities/REITs |

| Lock-in period | Fixed 5 years, any age | Until age 55, with 5+ years of contributions |

| Early exit | Allowed for specific reasons, 50% dividend forfeiture | Generally forfeits the tax credit, pays back waived taxes |

| Best for | Short-term, low-drama growth | Long-term retirement wealth with an upfront tax perk |

| Where to open | Virtual Pag-IBIG or any branch | Banks (BDO, BPI Wealth, UnionBank) or apps (DragonFi, Seedbox, GCash) |

A Quick Side-by-Side Example

Say you set aside ₱5,000 a month. Same amount, two accounts, two very different pictures.

Put it in MP2, using the 2025 declared rate of 7.12%. Your average balance across the year lands around ₱32,500, since your contributions build up gradually rather than sitting there all year. That works out to roughly ₱2,314 in dividends, tax-free, for that single year.

Put that same ₱60,000 a year into PERA instead, and you get an immediate ₱3,000 tax credit off your income tax bill, before your chosen fund even earns a single peso. A conservative bond fund might track close to MP2’s return. An equity fund could beat it in a strong year, or lag behind it in a weak one.

Neither figure is a promise. Both are illustrations, based on the actual rates and rules each program carried in 2025 and 2026. Real markets, and Pag-IBIG’s real performance, will move the actual results up or down from here.

PERA vs Pag-IBIG MP2

Two government-backed ways to grow your money. See how they actually differ, then run the numbers on your own contribution.

- What it is

- Government dividend savings program

- Best for

- Short-term, low-drama growth

- Where to open

- Virtual Pag-IBIG or any branch

- What it is

- Investment account, you pick the funds

- Best for

- Long-term retirement wealth with an upfront tax perk

- Where to open

- Banks (BDO, BPI Wealth, UnionBank) or apps (DragonFi, Seedbox, GCash)

*Lump sums over ₱500,000 require a Manager’s Check; amounts over ₱100,000 require proof of source of funds.

MP2 early exit is allowed for disability, retirement, permanent migration, layoff, OFW repatriation, death, or critical illness.

Run your own numbers

Estimates only, based on the 2025 declared MP2 rate (7.12%) and PERA’s 5% tax credit rule. Not a guaranteed return. General information, not personalized financial advice.

Impact

For the regular employee, MP2 feels familiar. It’s already tied to the same paycheck deductions you’re used to. Opening one takes minutes, not paperwork.

For the self-employed and freelancers, PERA fills a gap MP2 was never built for. No employer, no HR department quietly building a pension behind your back while you’re busy complaining about the pantry coffee. PERA becomes the closest substitute.

For OFWs, both options work. MP2 through Virtual Pag-IBIG, funded remotely. PERA through apps like DragonFi or GCash, with a contribution ceiling sized for remittance-driven income.

For the gig worker juggling Grab rides, food deliveries, and a side hustle, either account beats doing nothing. MP2 for the shorter horizon. PERA for the tax credit and the long game.

Which One Should You Choose

Consider MP2 if:

- You want a shorter commitment, five years instead of decades

- You’d rather not pick individual funds yourself

- You want a rate that’s historically outpaced regular bank savings

Consider PERA if:

- You want an immediate tax credit this filing season

- You’re comfortable choosing between bonds, equities, or REITs

- You’re building specifically for retirement, not a mid-term goal

Consider both if:

- Your budget has room for more than one

- You want short-term stability and long-term growth working at the same time

This isn’t financial advice tailored to your exact situation. It’s a starting point. Your own timeline, risk tolerance, and goals still make the final call.

Our Insight

MP2 wins the popularity contest for one simple reason. Almost every working Filipino already has a Pag-IBIG membership. Opening MP2 feels like flipping a switch on something that already exists.

PERA asks for one extra step. Pick an administrator. Choose a fund. Understand what a UITF is, which is about as thrilling as reading a data privacy policy, except this one has actual money attached. That small bit of friction is enough to make plenty of Filipinos skip it, even when the tax credit alone would beat MP2’s dividend in year one for higher earners.

None of this matters, though, if the explanation stays locked inside a BSP circular or an HDMF memorandum. Most Filipinos won’t read a 40-page implementing rule. They’ll read a Facebook post from their Tita, or a forward in the family Viber group, or an article written the way people talk: part English for the technical terms, part Filipino for the real talk. Reaching an OFW household in Cebu and a BGC office worker with the same explanation means writing for both realities at once, not just the one with a finance degree.

FAQ

PERA vs Pag-IBIG MP2: Your Questions Answered

Modified Pag-IBIG 2 is a voluntary savings program for active Pag-IBIG Fund members, with a fixed 5-year term and a dividend rate declared annually. The 2025 rate was 7.12%.

The Personal Equity and Retirement Account is a government investment program under Republic Act No. 9505 that gives contributors a 5% annual tax credit, tax-free growth, and tax-free withdrawal once they turn 55 with at least five years of contributions.

MP2’s declared rate has recently outpaced many conservative benchmarks, but it isn’t guaranteed year to year. PERA’s returns depend entirely on which fund you choose, and can land higher or lower than MP2 depending on market performance.

Yes. They have separate contribution limits and serve different purposes, so funding both isn’t redundant.

Both are open to OFWs. PERA offers a higher contribution ceiling (₱400,000/year) and matching tax credit for overseas workers, while MP2 requires only active Pag-IBIG membership and can be funded remotely through Virtual Pag-IBIG.

You can still withdraw early under specific valid reasons, such as disability, retirement, permanent migration, layoff, OFW repatriation, death, or critical illness, but doing so forfeits 50% of the dividends earned.

Generally no, not without giving up the tax benefits already claimed and paying back the taxes that were waived. Exceptions exist only for permanent disability or prolonged hospitalization.

MP2 carries lower risk since it’s a government-declared dividend rate rather than a market-linked investment. PERA’s risk depends entirely on which fund you pick, ranging from low-risk bonds to higher-risk equities and REITs.

Final Thoughts

Retirement rewards whoever starts, not whoever picked the bigger number. MP2 or PERA, five years or thirty, the account that grows your money is the one you opened.